EX-10.36

Published on September 2, 2022

EXHIBIT 10.36

ASSURANCE OF VOLUNTARY COMPLIANCE

This Assurance of Voluntary Compliance1 (the “Assurance”) is entered into by the Attorneys General of the States and Commonwealths of Alaska, Alabama, Arkansas, Arizona, California, Colorado, Connecticut, Delaware, Florida, Georgia, Illinois, Iowa, Idaho, Indiana, Kansas, Kentucky, Louisiana, Massachusetts, Maryland, Maine, Michigan, Minnesota, Missouri, Mississippi, Montana, North Carolina, North Dakota, Nebraska, New Hampshire, New Jersey, New Mexico, Nevada, New York, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Vermont, Washington, Wisconsin,

1 This Assurance of Voluntary Compliance shall, for all necessary purposes, also be considered an Assurance of Discontinuance. The Attorneys General have authority to execute this Assurance. See generally N.Y. Exec. Law § 63(15); Tenn. Code Ann. § 47-18-107; Florida Statutes Section 501.207(6); Illinois Consumer Fraud and Deceptive Business Practices Act, 815 ILCS 505/6.1; N.J.S.A. 56:8-1 to -227; P.A. Unfair Trade Practices and Consumer Protection Law 73 P.S. § 201-5; Tex. Bus. & Com. Code § 17.58; RCW 19.86.100; Alaska Stat. § 45.50.511; Ala. Code § 8-19-4; Arkansas Code Annotated § 4-88-114; Ariz. Rev. Stat. § 44-1530; C.R.S. § 6-1-110(2); Conn. Gen. Stat. § 42-110j; D.C. Code 28-3909(c)(6); 29 Del. C. § 2525(a) (authorizing cease and desist orders by agreement); O.C.G.A. § 10-1-402; Haw. Rev. Stat. Sect. 487-12; Iowa Code § 714.16 ; Iowa Admin. Code R. 61-38.1; Idaho Code § 48-610; Ind. Code § 24-5-0.5-7; Kentucky Revised Statutes 367.230; Unfair Trade Practices and Consumer Protection Law, La. R.S. § La. R.S. 51:1410; M.G.L. c. 93A, sec. 5.; Md. Code Ann., Com. Law § 13-402; 5 M.R.S.A. § 210; Mich. Comp. Laws § 445.906; Minn. Stat. § 8.31, subd. 2b; §407.030 RSMo; Mississippi Consumer Protection Act, MS Code Ann. §75-24-27(1)(g) ; Mont. Code Ann. § 30-14-112; N.D.C.C. 51-15-06.1; Neb. Rev. Stat. § 59-1610 and Neb. Rev. Stat. § 87-202.05(2); N.H. Rev. Stat. Ann. § 358-A:1-7; New Mexico Unfair Practices Act NMSA 1978, §57-12-9 (1971); Nev. Rev. Stat. 598.0995; Ohio Revised Code 1345.06(F); 15 O.S. § 756.1; ORS 646.632; R.I. Gen. Laws § 6–13.1–6 ; South Carolina Code § 39-5-60; SDCL 37-24-19; Utah Code § 13-2-1, et seq.; Va. Code Ann. § 59.1-202; 9 V.S.A. § 2459; Wis. Stat. § 100.18(11)(e); W. Va. Code § 46A-7-107; and Wyo. Stat. Ann. § 40-12-107.

This Assurance of Voluntary Compliance is a Settlement Agreement for the purposes of the North Carolina Unfair and Deceptive Practices Act, N.C. Gen. Stat. § 75-1.1 et seq.

The State of California is simultaneously entering into a settlement in a form consistent with the requirements of California law. That settlement incorporates the substantive terms of this Assurance and any differences between California’s settlement and this Assurance arise from the differences as to form.

The State of Connecticut is represented by the Connecticut Attorney General, acting at the request of the Commissioner of Consumer Protection. Conn. Gen. Stat. §§ 42-110j and 42-110m.

Hawaii is represented on this matter by its Office of Consumer Protection, an agency which is not part of the state Attorney General’s Office, but which is statutorily authorized to undertake consumer protection functions, including legal representation of the State of Hawaii. For simplicity purposes, the entire group will be referred to as the “Attorneys General” or individually as “Attorney General” and the designations, as they pertain to Hawaii, refer to the Executive Director of the State of Hawaii’s Office of Consumer Protection.

Maryland is represented by the Consumer Protection Division of the Office of the Attorney General of Maryland. For simplicity purposes, the entire group will be referred to as the “Attorneys General” or individually as “Attorney General” and the designations, as they pertain to Maryland, refer to the Consumer Protection Division of the Office of the Attorney General of Maryland. The Consumer Protection Division has authority to enter into this Assurance pursuant to Md. Code. Ann., Com. Law § 13-402.

Herein, no state-specific language or provision included in a footnote or appendix, or any state-specific portion thereof, shall affect the interpretation, construction, or enforcement of the Assurance with respect to any signatory State not referenced in such footnote or appendix, or any state-specific portion thereof.

Intuit understands each State may conform the form of the Assurance in accordance with statute, rule, or practice and may add a cover page, caption, or appendix to the document.

1

West Virginia, and Wyoming, the District of Columbia, and the Executive Director of the State of Hawaii Office of Consumer Protection (the “Attorneys General” or the “States”) and Intuit Inc. (“Intuit”; together with the “Attorneys General,” the “Parties”) to resolve an investigation of the Attorneys General into Intuit’s marketing, advertising, promotion, and sale of certain online tax preparation products and whether Intuit’s conduct constituted deceptive or unfair business acts or practices in violation of the States’ consumer protection laws.2 In consideration of their mutual agreements to the terms of this Assurance, and such other consideration as described herein, the sufficiency of which is hereby acknowledged, the Parties hereby enter into this Assurance and agree as follows:

DEFINITIONS

For the purpose of this Assurance, the following definitions apply:

A. “Advertisement” or “Advertising” means any written or verbal statement, illustration, or depiction that promotes the sale or use of a consumer good or service, or is designed to increase consumer interest in a brand, good, or service. Advertising media includes, but is not limited to promotional materials; print; television; radio; and Internet, Paid Display Advertisements, Paid Search Advertisements, display, social media, and other digital content.

2 See generally N.Y. Exec. Law § 63(12); N.Y. Gen. Bus. Law §§ 349-50; Tenn. Code Ann. §§ 47-18-104; Florida Deceptive and Unfair Trade Practices Act, Chapter 501, Part II, Florida Statutes; Illinois Consumer Fraud and Deceptive Business Practices Act, 815 ILCS 505/1, et seq.; N.C.G.S. § 75-1.1; N.J.S.A. 56:8-2; P.A. Unfair Trade Practices and Consumer Protection Law, 73 P.S. §§ 201-1 – 201-9.2; Tex. Bus. & Com. Code Ann. §§ 17.41 through 17.63; RCW 19.86.020; Alaska Stat. § 45.50.471; Ala. Code § 8-19-1 et seq.; Arkansas Code Annotated § 4-88-107(a); Ariz. Rev. Stat. §§ 44-1521 to 1534; Cal. Bus. & Prof. Code § 17200 et seq., § 17500 et seq.; C.R.S. § 6-1-101 et seq.; C.R.S. § 6-1-105(1); Conn. Gen. Stat. § 42-110b (a); D.C. Code 28-3904; 6 DEL. C. § 2513; O.C.G.A. § 10-1-390 et seq.; Haw. Rev. Stat. Chpts. 480 and 481A; Iowa Code § 714.16; Idaho Consumer Protection Act, title 48, chapter 6, Idaho Code; Ind. Code § 24-5-0.5-0.1, et seq.; K.S.A. § 50-623 et seq.; Kentucky Revised Statutes 367.170; Unfair Trade Practices and Consumer Protection Law, La. R.S. §§ 51:1401 et seq.; M.G.L. c. 93A, secs 2 & 4.; Md. Code Ann., Com. Law §§ 13-101 through 13-501; 5 M.R.S.A. § 205-A et seq; Mich. Comp. Laws § 445.903; Mich. Comp. Laws § 445.901 et seq.; Minn. Stat. §§ 325D.44; 325F.69, subd. 1; §407.020 RSMo; Mississippi Consumer Protection Act, MS Code Ann. §75-24-1 et seq.; Mont. Code Ann. § 30-14-103; N.D. Cent. Code § 51-15-01 et seq.; Neb. Rev. Stat. §§ 59-1601 to 59-1622 and Neb. Rev. Stat. §§ 87-301 to 87-306.; N.H. Rev. Stat. Ann. § 358-A:1-7; New Mexico Unfair Practices Act NMSA 1978, §57-12-1 et seq. (1967); NRS 598.0903 et al.; Ohio Consumer Sales Practices Act (“CSPA”), Ohio Revised Code 1345.01 et seq., and its Substantive Rules, 109-4-3-01, et seq. ; Oklahoma Consumer Protection Act, 15 O.S. §§ 751 et seq.; Oregon’s Unlawful Trade Practices Act, ORS 646.605 to 646.652; ORS 646.608(1)(b), (c), (e), and (s); R.I. Gen. Laws § 6–13.1–1 et seq.; South Carolina Code § 39-5-10 et seq.; SDCL Chapter 37-24; Utah Code § 13-11-4; Va. Code Ann. §§ 59.1-196 to 59.1-207; 9 V.S.A. § 2453; Fraudulent Representations. Wis. Stat. § 100.18(1); W. Va. Code §§ 46A-1-101, et seq.; Wyo. Stat. Ann. § 40-12-101 through -114 (the “Consumer Protection Acts”).

2

B. “Clearly and Conspicuously” means that a required disclosure is difficult to miss (i.e., easily noticeable) and easily understandable by ordinary consumers, including in all of the following ways:

1) In any communication that is solely visual or solely audible, the disclosure must be made through the same means through which the communication is presented. In any communication made through both visual and audible means, such as a television Advertisement, the disclosure must be presented in both the visual and audible portions of the communication even if the representation requiring the disclosure is made in only one means (the disclosures in the visual and audible portions of the communication in Space-Constrained Video Advertisements are not required to be identical).

2) A visual disclosure, by its size, contrast, location, the length of time it appears, and other characteristics, must stand out from any accompanying text or other visual elements so that it is easily noticed, read, and understood.

3) An audible disclosure, including by telephone or streaming video, must be delivered in a volume, speed, and cadence sufficient for ordinary consumers to easily hear and understand it.

4) In any communication using an interactive electronic medium, such as the Internet or software, the disclosure must be unavoidable.

3

5) The disclosure must use diction and syntax understandable to ordinary consumers and must appear in each language in which the representation that requires disclosure appears.

6) The disclosure must comply with these requirements in each medium through which it is received, including all electronic devices and face-to-face communications.

7) The disclosure must not be contradicted or mitigated by, or inconsistent with, anything else in the communication.

8) When the representation or sales practice targets a specific audience, such as children, the elderly, or the terminally ill, “ordinary consumers” includes reasonable members of that group.

C. “Close Proximity” means that the disclosure is very near the triggering representation and that the disclosure is made simultaneously with the triggering representation and remains or is repeated throughout the duration of the Advertisement. For example, a disclosure made through a hyperlink, pop-up, interstitial, or other similar technique is not in Close Proximity to the triggering representation.

D. “Effective Date” means the date on which all of the Parties have signed this Assurance.

E. “Intuit IRS Free File Product” means Intuit’s TurboTax Free File Program, TurboTax Freedom Edition, IRS Free File Program delivered by TurboTax or any other Intuit product or service that was or in the future may be provided pursuant to a memorandum of understanding or an agreement between Free File, Inc. (or any successor entity) and the IRS for the provision of free online tax preparation and e-filing services.

4

F. “Oversight Committee” shall mean the following Attorneys General: Florida, Illinois, New Jersey, New York, North Carolina, Pennsylvania, Tennessee, Texas, and Washington.

G. “Paid Display Advertisement” means an online Advertisement in which Intuit pays, or causes another to pay, to have an Advertisement displayed on a website and pays for the Advertisement, regardless of whether consumers click on the Advertisement.

H. “Paid Search Advertisement” means an online Advertisement in which Intuit pays, or causes another to pay, to have an Advertisement displayed with search engine results for a particular search term and pays for the Advertisement only when consumers click on the Advertisement.

I. “Covered Consumer” means any individual, or individuals if a joint return was filed, who in Tax Years 2016, 2017, or 2018 was (1) eligible to use an Intuit IRS Free File Product; (2) began his or her tax returns using a TurboTax Free Edition Product; (3) was informed that he or she was ineligible to use a TurboTax Free Edition Product; (4) subsequently paid to use a TurboTax Paid Product, and (5) had not used the Intuit IRS Free File Product in a previous tax year.

J. “Space-Constrained Advertisement” means any online Advertisement (including but not limited to Paid Display Advertisements and Paid Search Advertisements) or any Video Advertisement that has space, time, format, size, or technological restrictions that limit Intuit from being able to make the disclosures required by this Assurance. Intuit bears the burden of showing that there is a constraint or insufficient space and time to make a required disclosure that is Clear and Conspicuous and in Close Proximity to the triggering term. Space-Constrained Advertisements do not include Advertisements on a TurboTax Website.

5

K. “TurboTax Free Edition Product” means any online software product offered by Intuit that allows consumers, without paying a fee, to prepare and file federal tax returns, state tax returns, or both, including but not limited to “TurboTax Free Edition” and “Federal Free Edition.” “TurboTax Free Edition Product” does not include any Intuit IRS Free File Product, any TurboTax Paid Product, TurboTax Live, or any products sold or offered within the TurboTax Free Edition Product, such as Audit Defense.

L. “TurboTax Paid Product” means the online tax preparation software products offered by Intuit that allow consumers, for a fee, to prepare and file federal tax returns, state tax returns, or both, for themselves. “TurboTax Paid Product” does not include products sold or offered in addition to a TurboTax Paid Product.

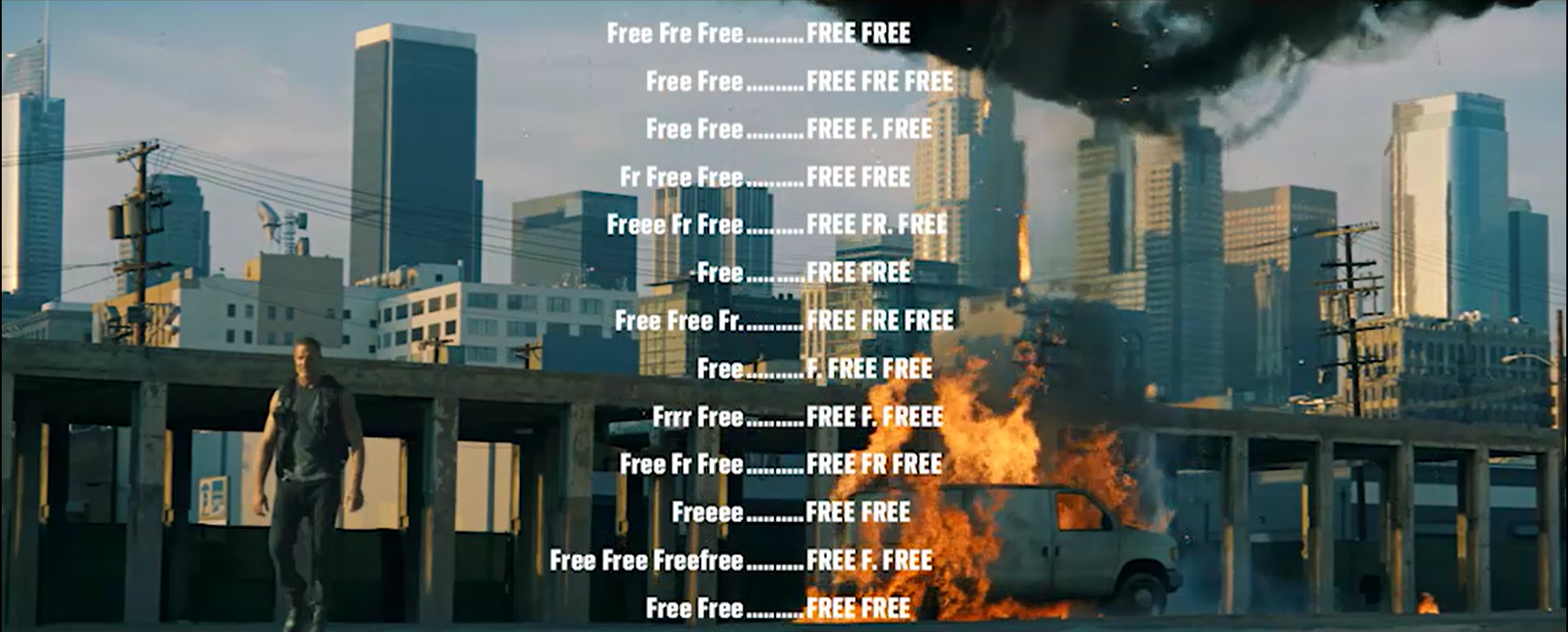

M. “TurboTax Website” means turbotax.intuit.com, any subdomain of turbotax.intuit.com, and any other website owned, operated, or controlled partially or wholly by Intuit that provides or offers TurboTax Paid Products or TurboTax Free Edition Products.

N. “Upgrade Screen” means any display within the product flow of the TurboTax Free Edition Product that appears when consumers using that product indicate they have income, credits, deductions, or other tax situations not covered by the TurboTax Free Edition Product, and offers consumers the option of using a TurboTax Paid Product to prepare and file their federal and/or state tax returns.

O. “Video Advertisement” means any Advertisement made via television or made online using video.

FINDINGS

1. Intuit is a Delaware corporation with its principal place of business in Mountain View, California.

6

2. Intuit transacts or has transacted business in each State and throughout the United States. At all times relevant to this Assurance, acting alone or in concert with others, Intuit has advertised, marketed, distributed, or sold TurboTax, a tax preparation software that enables users to prepare and file their taxes through the internet, to consumers throughout the United States.

I. Intuit’s Free TurboTax Products

3. From at least 2016 to October 2021, Intuit offered two TurboTax online tax filing products that were available for free to consumers who met certain eligibility requirements. Each of these products had different eligibility requirements.

A. TurboTax’s “Freemium” Product: TurboTax Free Edition

4. Since at least 2016, Intuit has engaged in what it calls a “freemium” business strategy that monetizes free products.

5. This “freemium” business strategy involves, in part, growing Intuit’s customer base by offering free products to consumers to whom Intuit sells separate add-on products and inducing customers to upgrade to paid versions of TurboTax.

6. Since at least 2017, Intuit has called its “freemium” product “TurboTax Free Edition.” In 2016, Intuit called its “freemium” product “Federal Free Edition.”

7. This TurboTax “freemium” product is only available to consumers with “simple” tax returns, as defined by Intuit; other consumers are required to upgrade to paid products to file through Intuit.

8. For consumers filing their 2016 and 2017 taxes, Intuit defined a “simple” tax return as a return that could be filed using a 1040A or 1040EZ tax form.

9. Since 2019, when consumers filed tax returns for Tax Year (“TY”) 2018 income, Intuit has defined a “simple” tax return as a return that could be filed on a Form 1040, with no attached schedules, regardless of the consumer’s income.

7

B. Intuit’s Free File Product

10. From 2003 to October 2021, Intuit offered a free version of its online tax preparation products through its participation in the United States Internal Revenue Service (“IRS”) Free File Program, a public-private partnership formed in 2002 between a consortium of tax preparation software companies and the IRS pursuant to a Memorandum of Understanding (“MOU”). Under the MOU, participating companies offer free online tax preparation products to low- and middle-income Americans. In exchange, the IRS agreed not to compete with the participating companies in providing free, online tax return preparation and filing services to American consumers.

11. Historically, consumer participation in the IRS Free File Program has been low.

12. The IRS has set eligibility thresholds for participation in the Free File Program based on consumers’ adjusted gross income (“AGI”). Consumers with an AGI equal to or less than 70% of the U.S. consumer population are meant to be eligible for the program. The MOU, however, requires that no company offer its Free File product to more than 50%, or less than 10%, of eligible consumers. Each company is free to set its own eligibility requirements to stay within that range.

13. From 2017 (filings on TY 2016 income) to 2021 (filings on TY 2020 income), Intuit made its Free File product available to all consumers who were eligible for the earned income tax credit.

14. From 2017 to 2021, Intuit also made its Free File product available to all consumers with an AGI that does not exceed specified AGI thresholds:

8

| Tax Year | Maximum AGI | ||||||||||

| 2016 (returns filed in 2017) | $33,000 | ||||||||||

| 2017 (returns filed in 2018) | $33,000 | ||||||||||

| 2018 (returns filed in 2019) | $34,000 | ||||||||||

| 2019 (returns filed in 2020) | $36,000 | ||||||||||

| 2020 (returns filed in 2021) | $39,000 | ||||||||||

15. From 2017 to 2021, Intuit also made its Free File product available to all active duty military service members with an AGI that does not exceed specified AGI thresholds:

| Tax Year | Maximum AGI | ||||||||||

| 2016 (returns filed in 2017) | $64,000 | ||||||||||

| 2017 (returns filed in 2018) | $66,000 | ||||||||||

| 2018 (returns filed in 2019) | $66,000 | ||||||||||

| 2019 (returns filed in 2020) | $69,000 | ||||||||||

| 2020 (returns filed in 2021) | $72,000 | ||||||||||

16. Although consumers primarily accessed Intuit’s Free File product via IRS.gov, they have also accessed it directly via Intuit’s internet landing page for the product, which is different from the landing page for its “freemium” and paid products.

17. Intuit changed the name of its Free File product several times. Intuit also used different names for its Free File product at the same time, depending on where the product was being marketed.

18. Prior to TY 2018, Intuit called its Free File product “TurboTax Freedom Edition.”

9

19. For TY 2018, Intuit changed the name of its Free File product to “TurboTax Free File Program.”

20. From at least TY 2016 through and including TY 2018, Intuit used a different name to market its Free File product on the IRS.gov website. On the IRS.gov website, Intuit marketed its Free File product as “TurboTax All Free ℠.”

21. For TY 2019 and 2020, Intuit changed the name of its Free File product to “IRS Free File Program Delivered by TurboTax.” This change was required by an amendment to the MOU between the IRS and the participating tax preparation companies that required uniform naming of all IRS Free File Program products.

C. The Tension Between Intuit’s Free File and “Freemium” Products

and Related Consumer Confusion

and Related Consumer Confusion

22. Intuit’s Free File product yielded benefits to the company as part of its efforts to avoid government “encroachment” into the tax preparation industry.

23. Indeed, Intuit has acknowledged publicly the competitive threat of a government-run free e-filing system, including in Securities and Exchange Commission filings.

24. Intuit has recognized that high participation in the IRS Free File Program would dent its bottom line, but that, at the same time, it had to keep Free File enrollments above a certain level to prevent government “encroachment.”

25. For several years prior to TY 2018, Intuit employees tasked with overseeing the marketing strategy for both Intuit’s Free File and “freemium” products considered changing the name of Intuit’s Free File product.

26. Intuit knew that consumers were confused by the similarity of the names of these products. Intuit chose to name its commercial freemium product TurboTax “Free Edition,” even though it is only free for approximately one-third of taxpayers, while it named its Free File

10

product “Freedom Edition,” which does not indicate that it is free despite being part of a program that is free for 70 percent of taxpayers.

27. In 2018, Intuit knew that consumers were still confused about the differences between its Free File and “freemium” products.

28. Although Intuit changed the name of its Free File product to TurboTax Free File Program for TY 2018, it continued to market its Free File product on the IRS.gov website using the trademarked name TurboTax All Free. Moreover, Intuit was aware that changing the name to TurboTax Free File Program would not create any additional clarity for its customers and that consumers would be confused between the Free File Program and TurboTax Free Edition, especially due to the company’s focus on the use of “free” in marketing its products.

29. In 2019, this time pursuant to the MOU with the IRS, Intuit again changed the name of its Free File product, renaming it to IRS Free File Program Delivered by TurboTax.

II. Online Search Practices

A. For TY 2018, Intuit Hid Its Free File Landing Page from Search Engines for

Approximately Five Months During the Peak of Tax Season

Approximately Five Months During the Peak of Tax Season

30. In 2018, Intuit employees responsible for marketing strategy feared the name change of Intuit’s Free File product could negatively impact the ranking of the company’s “freemium” product in online search engine results, leading to a loss in revenue.

31. For TY 2018, Intuit blocked the landing page for its newly named Free File product so that it would not be indexed (listed) by internet search engines. That block was in place from November 13, 2018, to April 26, 2019. This timeframe covered the vast majority of Intuit’s 2019 tax filing season, which is the time it received revenue from consumers using TurboTax products to file tax returns for TY 2018.

11

32. For TY 2019, Intuit stopped blocking its Free File product landing page from online search engines, and 2,070,778 consumers filed their federal tax returns using Intuit’s Free File product, representing growth of 73% over TY 2018.

B. Intuit Used Paid Search Terms to Direct Consumers Searching for the

IRS Free File Program to Intuit’s “Freemium” and Paid Products

IRS Free File Program to Intuit’s “Freemium” and Paid Products

33. As part of its advertising and marketing practices, Intuit has bid on paid search terms with search engines such as Google and Bing. When a consumer queried a search engine for a search term and Intuit won the search engine’s instant auction for that paid search term, the consumer would be served an ad selected by Intuit that included a hyperlink directing the consumer to a specific website.

34. For many years, including TY 2018 while Intuit had blocked the landing page for its Free File product from appearing in online search results, Intuit bid on search terms relevant to the IRS Free File Program.

35. In many instances, these search terms indicated consumers were likely searching for information about, or links to reach the website for, the IRS Free File Program. For example, Intuit bid on the following 13 search terms:

|

free file

free file irs

free file taxes

free file taxes online

free file turbotax

free file turbo tax

irs free file

|

irs.gov/freefile

irs.gov/freefile.

irs.gov free file

irs.gov/free file

turbo tax free file

turbotax free file program

|

||||

36. For each of the 13 search terms referenced in paragraph 35, during TY 2018—while Intuit had blocked the landing page for its Free File product from appearing in search results—Intuit’s online ads directed consumers to Intuit’s commercial website with its

12

“freemium” product, rather than the IRS.gov website for the IRS Free File Program or the landing page for Intuit’s Free File product.

37. During TY 2018, Intuit directed consumers towards the website for “freemium” and paid products when consumers searched for its Free File product by its exact name: Turbo Tax Free File Program.

38. If a taxpayer knew to type “TurboTax Freedom” in a search engine, she would receive a paid advertisement which, during the 2019 filing season, would direct her to a landing page with a button link that said “See If You Qualify” that eventually lead to the Freedom Edition website. However, the landing page also included a prominent link that said “Start for Free,” which directed the user to TurboTax’s commercial and paid products.

39. Intuit knew that some of its customers were misled by these practices.

III. Advertising Practices: Intuit’s Advertisements Misrepresented that Consumers Were Eligible for a Free Version of Its Products

40. Since at least 2016, Intuit has extensively promoted its TurboTax products through advertising in a variety of mediums touting that it offers a free service.

41. Among its “do-it-yourself” online software products, Intuit used ads, including television and social media ads, to promote its “freemium” TurboTax product.

42. Intuit also has engaged in an ad campaign it calls “Free, Free, Free” in which “free” is essentially the only word spoken by the actors in the commercials, until the voice over at the end of the advertisement. Intuit used at least six different advertisements in this campaign.

43. Many of Intuit’s ads contain a fine print disclaimer at the end of the commercial informing consumers that the offer is limited to consumers with “simple tax returns” or “simple U.S. returns only.” This fine print disclaimer was not conveyed audibly.

13

44. The disclaimers are inadequate to cure the express representation that the advertised products are free.

45. A reasonable consumer could believe that the products Intuit advertises as free are free for them, given that online products in many industries, including in online tax preparation, are routinely offered to consumers completely free of any charge.

46. Intuit’s false statements or representations that TurboTax is free, without adequately disclosing the limitations of its free offer, have induced consumers to begin using TurboTax and, after discovering they are not eligible for Intuit’s “freemium” product (as described below), to pay for paid TurboTax products.

IV. Website Practices

A. Intuit’s TurboTax Home Page Misled Consumers into Believing

They Were Eligible for Its “Freemium” Product

They Were Eligible for Its “Freemium” Product

47. When consumers who saw Intuit’s advertisements visited the TurboTax website, the website’s home page failed to adequately disclose the limitations on eligibility for Intuit’s “freemium” product.

48. For example, for TY 2018, the TurboTax home page contained a screen that mimicked the “free, free free free” ad campaign.

49. The screen failed to disclose adequately the limitations on eligibility.

50. Consumers who proceeded with the “freemium” product would be brought to a login screen and then start an online, automated “interview” to begin entering information to file their taxes. Consumers who were not eligible for Intuit’s “freemium” TurboTax product would not learn they were ineligible until they had already invested significant time and effort creating an account and inputting their personal tax information into the TurboTax product.

14

51. For TY 2019, the TurboTax home page used a similar screen, with an even greater emphasis that consumers were “guaranteed” a free product. Again, consumers who were not eligible for Intuit’s “freemium” TurboTax product would not learn they were ineligible until they had already invested significant time and effort creating an account and inputting their personal tax information into the TurboTax product.

52. For TY 2020 and 2021, Intuit has continued to employ a customer interview model in which consumers who were not eligible for Intuit’s “freemium” TurboTax product would not learn they were ineligible until they had already invested significant time and effort creating an account and inputting their personal tax information into the TurboTax product.

B. Intuit’s TurboTax Products and Pricing Screen Failed to Disclose Intuit’s Free File Product, Further Impeding Consumers from Learning of Its Existence

53. Intuit’s TurboTax website has featured a screen Intuit calls its “Products and Pricing” screen. For TY 2018, the headline on this screen informed consumers: “Tell us about you – we’ll recommend the right tax solution.”

54. When consumers clicked on one of the options on this screen, the TurboTax website would then recommend one of four products: (1) its “freemium” product, marketed as Free Edition; (2) Deluxe; (3) Premier; or (4) Self-Employed—the latter three being Intuit’s paid do-it-yourself tax products. At the bottom of the screen, all four products were displayed, with the recommended product highlighted.

55. This screen never displayed or recommended the TurboTax Free File product to consumers, even when they were ineligible for the “freemium” product, TurboTax Free Edition.

56. In fact, in TY 2019, the TurboTax website had a site index at the bottom of the home page with a link to “All online tax preparation software.” That link brought consumers to the Products and Pricing screen, which did not disclose Intuit’s Free File product. Likewise,

15

during TY 2020, the TurboTax app contained a similar list of “all products” that did not include Intuit’s Free File product.

57. For eligible consumers based on their AGI, Intuit’s former Free File product covered all tax situations, forms, and deductions, thus providing coverage equal to Intuit’s most expensive TurboTax online product, Self-Employed.

C. The TurboTax Interview Process Used “Hard Stops” to Induce

Consumers to Upgrade from Free to Paid Products

Consumers to Upgrade from Free to Paid Products

58. Intuit represented to consumers who are not eligible for the “freemium” product that they must provide their payment information and pay Intuit in order to file their tax returns online with TurboTax, even if the consumer was eligible to file for free through Intuit’s former Free File product. Intuit informed consumers of these required upgrades using screens its employees call “Hard Stops.” Intuit still employs Hard Stops in its “freemium” product.

59. When consumers use the TurboTax “freemium” product, Intuit’s software asks them a series of questions on successive webpages about their financial situation. These questions enable Intuit to determine whether consumers are eligible for the “freemium” product and include, among other things, whether the consumer paid student loan interest or was self-employed.

60. After supplying the information, consumers are prompted to input their income by category. When consumers indicate that they need to report income on a Form 1099-MISC (for example, because entities that paid them classified them as independent contractors), the TurboTax “freemium” product displays a Hard Stop informing them that they cannot proceed for free. For example, Intuit’s TY 2019 “Business Income Upgrade” Hard Stop told consumers: “To accurately report this income, you’ll need to upgrade.”

16

61. Hard Stop screens then offer consumers the option to upgrade and pay for a paid TurboTax product, such as TurboTax Deluxe or TurboTax Self-Employed. At various times during TY 2018 and 2017, Intuit charged $59.99 for TurboTax Deluxe and $119.99 for TurboTax Self-Employed.

62. The Business Income Hard Stop was likely to deceive or mislead consumers who were eligible for Intuit’s former Free File product.

63. The headline in the Business Income Hard Stop states that consumers must upgrade to a paid product to “accurately report this income.” That statement was false at the time for a large percentage of TurboTax customers—those who were eligible for Intuit’s Free File product.

64. The Business Income Hard Stop was also misleading because it included a button that says “keep free” below the column for TurboTax Free Edition, even though the consumer could not actually continue using TurboTax Free Edition and report all of her income to the IRS.

65. Upon clicking on the “keep free” button, consumers were put into a feedback loop that ended only if they upgraded to a paid product or chose not to report their 1099 income.

66. Intuit has used and is using many other Hard Stops to induce consumers to upgrade based on certain types of income, such as income from a farm, farm rental or farm equipment; selling a home; a prior year state tax refund; or investments. All of these Hard Stops misled consumers eligible for Intuit’s former Free File product to provide their payment information and buy paid TurboTax products.

67. Overall, for all Hard Stops from TY 2016 through TY 2018, millions of consumers started in “freemium,” encountered a Hard Stop, and then upgraded to and filed in a paid product. Many of those who were shown a Hard Stop were eligible at the time for Intuit’s

17

Free File product. These Free File-eligible consumers who upgraded in response to a Hard Stop paid Intuit more than $100 million to file their federal tax returns.

68. From at least 2017 to October 2021, when consumers encountered these Hard Stops, Intuit failed to disclose to consumers that they may have been or were eligible to use Intuit’s Free File product to accurately report their income or claim certain tax deductions.

V. Conclusion

69. Based on these Findings, the Attorneys General have reason to believe that Intuit has engaged in deceptive and unfair acts and practices in violation of the States’ Consumer Protection Acts, in the marketing, advertising, promotion, and sale of online tax preparation products.

70. Intuit voluntarily withdrew from the IRS Free File Program effective October 2021 and would be able to seek to rejoin the IRS Free File Program at any time but for the provisions of this Assurance. Intuit could not rejoin the IRS Free File Program without approval of the IRS and the Director of the Free File Alliance.

71. Solely for purposes of this Assurance, Intuit neither admits nor denies any of the Findings in paragraphs 3 through 70 of this Section.

INJUNCTIVE RELIEF

I. General Compliance

Intuit shall comply with the Consumer Protection Acts and any amendments to those laws, regulations, and rules that may be adopted by the States subsequent to the Effective Date of this Assurance.

II. Prohibition Against Misrepresentations

Intuit, Intuit’s officers, agents, employees, and attorneys, and all other persons in active concert or participation with any of them, who receive actual notice of this Assurance, whether

18

acting directly or indirectly, in connection with promoting or offering any online tax preparation products, must not misrepresent, expressly or by implication:

A. That consumers can only file their taxes online accurately if they use a TurboTax Paid Product or TurboTax Free Edition Product.

B. That consumers can only claim a tax credit or tax deduction if they use a TurboTax Paid Product or TurboTax Free Edition Product.

C. That consumers must upgrade to a TurboTax Paid Product to file their taxes online if they are eligible to use the TurboTax Free Edition Product.

D. That consumers can continue using and file their taxes for free with the TurboTax Free Edition Product when that is not the case, including by stating expressly or impliedly to consumers on an Upgrade Screen that they can continue using the TurboTax Free Edition Product through a “keep free” button or another button using similar language. Intuit may give consumers the option of continuing to use the TurboTax Free Edition Product on an Upgrade Screen, so long as a disclosure is made, Clearly and Conspicuously on the Upgrade Screen and in Close Proximity to any button, link, or option on the Upgrade Screen that permits the consumer to exercise the option of continuing to use the TurboTax Free Edition Product, that the current tax information entered by the consumer indicates that the consumer will need to upgrade to a TurboTax Paid Product to file his or her taxes.

E. Any other fact material to consumers concerning any tax preparation product or service, such as the price; total cost; any material restrictions, limitations, or conditions; or any material aspect of its performance, efficacy, nature, or central characteristics.

19

III. Required Disclosures and Business Practices for Advertising and Marketing of Free Products

As soon as reasonably practicable, but no later than August 1, 2022, in connection with advertising, marketing, promoting, offering, naming, or describing, or assisting in the advertising, marketing, promotion, offering, naming, or describing of any tax preparation products as free, whether directly or indirectly, Intuit must make the following disclosures about taxpayer eligibility for such free products and comply with the following terms:

A. In any non-Space-Constrained Advertisement of free tax preparation products other than on a TurboTax Website, Intuit must disclose, Clearly and Conspicuously, and in Close Proximity to the representation that the product is free: (1) the existence and category of material limitations on a consumer’s ability to use that free product; and (2) that not all taxpayers qualify for the free product.

B. In any Space-Constrained Advertisement of free tax preparation products other than Space-Constrained Video Advertisements, Intuit must disclose that eligibility requirements apply. If made online, Intuit must also (1) Clearly and Conspicuously include a hyperlink to a landing page or webpage on a TurboTax Website that Clearly and Conspicuously contains full disclosure of all material eligibility restrictions or (2) link by clicking on the Advertisement itself to a landing page or webpage on a TurboTax Website that Clearly and Conspicuously sets forth full disclosure of all material eligibility restrictions.

C. For a period of ten (10) years, in any Space-Constrained Video Advertisements of free tax preparation products, Intuit must visually disclose, Clearly and Conspicuously, and in Close Proximity to the representation that the product is free: (1) the existence and category of material limitations on a consumer’s ability to use that free product; and (2) that not all taxpayers qualify for the free product. In addition, for a period of ten (10) years, in any Space-Constrained

20

Video Advertisements of free tax preparation products except for such Advertisements that are 8 seconds or shorter, Intuit must verbally disclose, Clearly and Conspicuously and in Close Proximity to the representation that the product is free, that not all taxpayers qualify.

D. In any Advertisement of free tax preparation products on a TurboTax Website, and any space on a TurboTax Website listing, describing, offering, or promoting such free products, Intuit must disclose (1) Clearly and Conspicuously and very near to the representation all material limitations on a consumer’s ability to use that free product, including, but not limited to, eligibility criteria for that free product, or (2) through a hyperlink (i) that is very near to the representation, (ii) that indicates that there are material limitations on a consumer’s ability to use that free product, and (iii) that links to a landing page or webpage that Clearly and Conspicuously sets forth all material limitations on a consumer’s ability to use that free product, including, but not limited to, eligibility criteria for that free product.

E. Intuit must disclose Clearly and Conspicuously to consumers, at the earliest point at which it is reasonably possible to determine, that they do not qualify to file a tax return for free with the TurboTax Free Edition Product.

F. Intuit must take reasonable steps to design all TurboTax products to inform, at the earliest point it is reasonably possible, consumers using the TurboTax Free Edition Product whether they will or will not be able to file for free using that product.

G. Intuit must not publish, or cause to be published, in any medium (1) its “free, free, free” Video Advertisements (see Appendix A for a list of such advertisements) and (2) Video Advertisements that are substantially similar in their repetition of the word free. Intuit must comply with this Section III.G immediately upon the Effective Date, notwithstanding any contradictory language in the introduction to Section III above.

21

IV. Prohibition Against Data-Clearing Practices

Effective December 1, 2022, Intuit must permit consumers who enter a TurboTax Paid Product through an Upgrade Screen to return to the TurboTax Free Edition Product without being required to re-enter the data they provided when using the TurboTax Free Edition Product.

V. Voluntary Withdrawal From and Injunction Against Rejoining the IRS Free File Program

In recognition of Intuit’s voluntary withdrawal from the IRS Free File Program effective October 2021 and Intuit’s representation and commitment that it will not rejoin the IRS Free File Program, and in lieu of this Assurance containing specific injunctive provisions concerning Intuit’s potential future participation in the IRS Free File Program and conduct related thereto:

A. Intuit must not seek to rejoin or participate in the IRS Free File Program.

B. This term may only be modified by amending this Assurance pursuant to Section XII(H).

VI. Payment to the Settlement Fund and Administration Fund

A. Within thirty (30) days of the Effective Date, Intuit shall pay the total sum of One Hundred Forty-One Million Dollars ($141,000,000)3 (the “Required Payment”) as described herein. The Required Payment shall be made in two installments: (1) the first payment, in the amount of Two Million Five Hundred Thousand Dollars ($2,500,000) (the “Administration Fund”), shall be made by Intuit to an account for the payment of costs and expenses incurred or charged by the Fund Administrator in administering the Settlement Fund; (2) the second payment, in the amount of One Hundred Thirty-Eight Million Two Hundred and Fifty Thousand Dollars ($138,250,000) (the “Settlement Fund”), shall be made by Intuit to an account for the use of the fund administrator selected by the Oversight Committee (the “Fund Administrator”), for

3 From this amount, a total of Two Hundred and Fifty Thousand Dollars ($250,000) will be allocated for fees and costs to a certain previously designated State. This Two Hundred and Fifty Thousand Dollars ($250,000) will be paid into the Settlement Fund by Intuit and will distributed by the Oversight Committee.

22

the purpose of providing restitution to Covered Consumers as described hereunder, who shall be responsible for the administration of the Settlement Fund. The Required Payment installments shall be made by wire transfer in accordance with instructions provided by the Oversight Committee. After transfer of the Required Payment, Intuit shall have no right, title, interest or other legal claim in the transferred funds.

B. The Oversight Committee shall have sole discretion concerning the administration and distribution of the Settlement Fund, which may include determining the Covered Consumers who are entitled to payments from the Settlement Fund; the nature, timing, and amount of such payment; directing the Fund Administrator to make payments to these consumers; the timing and content of communications from the Fund Administrator to Covered Consumers concerning the Settlement Fund; directing the Fund Administrator to make payments of fees or costs from the Settlement Fund to one or more Attorneys General; and transferring funds from the Settlement Fund to the Administration Fund. Attached for informational purposes only as Appendix C is a preliminary calculation of each States’ percentage of the total population of Covered Consumers; the Oversight Committee is not required to distribute the Settlement Fund according to these preliminary percentages. If the Oversight Committee directs the Fund Administrator to make a payment of fees or costs to a State, that payment shall be deducted from the share of the Settlement Fund that is allocated to that State. Individual States may, at their discretion, append a State-specific appendix to their copy of this Assurance that sets forth the payment from the Settlement Fund that has been allocated to the Covered Consumers in that State and any payment of fees or costs to that State.

C. All costs and expenses incurred or charged by the Fund Administrator in administering the Settlement Fund shall be paid out of the Administration Fund. The Oversight

23

Committee shall have sole discretion concerning the administration and distribution of any money that remains in the Administration Fund after payment of all costs and expenses incurred or charged by the Fund Administrator in administering the Settlement Fund. In no event shall the Attorneys General be liable for any costs associated with administering the Settlement Fund. The administration of the Settlement Fund shall, include, but not be limited to, the following:

1. Identifying the current mailing address of each Covered Consumer, which shall be provided by Intuit and/or through the use of publicly-available databases, commercially-available databases, and public records;

2. Preparing and sending, by mail and email, communications to Covered Consumers relating to the settlement, including notice of the settlement and reminder notices to all Covered Consumers who had been sent a check but not yet cashed it;

3. Distributing restitution to each Covered Consumer by check, and reissuing checks as necessary, including for checks that have been returned;

4. Establishing a process by which Covered Consumers may elect to receive their payments through an electronic payment processor such as Venmo, PayPal, or Zelle instead of by check;

5. Maintaining a website that contain the terms and conditions of the settlement;

6. Providing and hosting a toll free number to provide information to Covered Consumers relating to the settlement during distribution of the restitution;

7. Contacting, by mail, email, or phone, Covered Consumers regarding uncashed checks;

24

8. Reporting to the Oversight Committee on the status of the administration of the Settlement Fund and responding to requests by the Oversight Committee for documentation and information necessary to confirm the proper administration of the Settlement Fund; and

9. Providing all other services necessary for the proper administration of the Settlement Fund.

D. Within sixty (60) days of the Effective Date, Intuit must submit to the Oversight Committee for review and non-objection its proposed contract with the Fund Administrator that includes a comprehensive Statement of Work consistent with Section VI.C and all other terms of this Assurance. The Oversight Committee will have the discretion to make a determination of non-objection to the Statement of Work or direct Intuit to revise it. If the Oversight Committee directs Intuit to revise the Statement of Work, Intuit must revise and resubmit the contract to the Oversight Committee within thirty (30) days. After receiving notification that the Oversight Committee has made a determination of non-objection to the Statement of Work, Intuit and the Settlement Administrator must implement and adhere to the steps, recommendations, deadlines, and timeframes outlined in the Statement of Work.

E. Intuit shall promptly provide the Fund Administrator (and the Oversight Committee, if requested by the Oversight Committee) with all information the Oversight Committee deems necessary to permit the Fund Administrator to distribute funds to Covered Consumers as directed by the Oversight Committee, including, but not limited to, the following for each consumer: full name; last known and prior mailing addresses, email addresses, and telephone numbers; and for each of Tax Years 2016, 2017, and 2018, the TurboTax Paid Product used by the consumer, if any, the amount the consumer paid to Intuit for said TurboTax Paid

25

Product, and the amount of any credits, chargebacks, or settlement amounts already paid by Intuit or received by such consumer for the TurboTax Paid Product. In carrying out the foregoing, Intuit agrees to provide such information as soon as possible but in no event more than thirty (30) calendar days of the Oversight Committee’s request.

F. Intuit shall warrant to the Oversight Committee at the time of supplying information to the Fund Administrator that the information is complete and accurate to the best of its knowledge and capability. Intuit’s duty to provide complete and accurate information regarding Covered Consumers shall continue throughout the administration process.

G. After the Fund Administrator has completed the administration of the Settlement Fund (including making reasonable attempts to contact payees of uncashed checks and waiting a reasonable period of time not less than ninety (90) calendar days), all uncashed checks may be voided. Once such uncashed checks have been voided, these funds shall be distributed to state unclaimed property funds, to any other fund or agency if so required by law, or to any other fund

26

or agency as lawfully directed by the Attorney General of the respective state,4 based on the last known state residence of the payee. The Fund Administrator must distribute uncashed funds, or any other remaining funds in the Settlement Fund, pursuant to instructions provided by the Oversight Committee.

H. Covered Consumers who receive a payment from the Settlement Fund shall not be required to return or discontinue the use of any Intuit goods or services, and receipt of any such payment shall not be tied to any other commitment.

4 For Arizona: Any funds distributed to the Arizona Attorney General’s Office shall be deposited into the Consumer Restitution and Remediation Revolving Fund, pursuant to A.R.S. § 44-1531.02(B). The Arizona Attorney General’s Office will have sole discretion as to how and when restitution funds are distributed to consumers. In the event that any portion of those funds is not distributed to eligible consumers, such portion will be deposited by the Arizona Attorney General’s Office into the Consumer Protection-Consumer Fraud Revolving Fund, pursuant to A.R.S. § 44-1531.02(B), and used for the purposes specified in A.R.S. § 44-1531.01.

For Colorado: Intuit shall pay to the Colorado Attorney General the total amount of any and all refund amounts that remain outstanding, whether because they were returned as undeliverable, unclaimed, uncashed, undeposited, or otherwise. For any such payments to the Colorado Attorney General, they shall be in the form of a certified check, cashier’s check, or money order made payable to the “Colorado Department of Law,” shall reference “Intuit-TurboTax” and shall be delivered to: Emily Lujan, Program Assistant, Consumer Protection Section, Colorado Department of Law, 1300 Broadway, 7th Floor, Denver, Colorado 80203. Such payments shall be held, along with any interest thereon, in trust by the Colorado Attorney General to be used in the Colorado Attorney General’s sole discretion for reimbursement of attorneys’ fees and costs, the payment of consumer restitution, if any, and for consumer or creditor educational purposes, for future consumer credit or consumer protection enforcement, or public welfare purposes.

For Delaware: All payments to the Delaware Attorney General pursuant to this Assurance shall be made to the Consumer Protection Unit of the Delaware Department of Justice (“CPU”). The CPU shall place all funds received in the State of Delaware's Consumer Protection Fund, and such funds may be utilized for any lawful purpose.

For New Mexico: For those funds allocated to New Mexico, such funds shall be directed to the New Mexico Office of the Attorney General’s (“NMOAG’s”) consumer settlement fund. The funds shall be expended, at the sole discretion of the NMOAG, (i) to enhance the NMOAG’s law enforcement efforts to prevent and prosecute elder fraud, consumer fraud, and/or other unfair or deceptive acts or practices, (ii) to investigate, enforce, and prosecute other illegal conduct related to deceptive online advertising, deceptive use of “dark patterns,” and/or violations of other consumer protection laws, and/or (iii) for any other lawful purpose, at the sole discretion of the NMOAG.

For Ohio: After the Fund Administrator has completed the administration of the Settlement Fund (including making reasonable attempts to contact payees of uncashed checks and waiting a reasonable period of time not less than ninety (90) calendar days), all uncashed checks may be voided. Once such uncashed checks have been voided, these funds shall be distributed and delivered to the office of the Ohio Attorney General. The money received by the office of the Ohio Attorney General pursuant to this paragraph may be used by the office of the Ohio Attorney General for purposes that may include, but are not limited to, attorney’s fees and other costs of investigation and litigation, or may be placed in, or applied to, any consumer protection law enforcement fund, consumer education, litigation or local consumer aid fund, or for such other uses permitted by Ohio law, at the sole discretion of the Ohio Attorney General.

For Washington: The total amount of any and all uncashed checks that had been direct to a payee whose last known residence was in the State of Washington that remain outstanding shall be paid to the Washington Attorney General’s Office. For any such payments to the Washington Attorney General, they shall be made in good funds by wire transfer or valid check payable to “State of Washington Attorney General’s Office,” delivered to the Office of the Attorney General, Attention: Margaret Farmer, Litigation Support Manager, 800 Fifth Avenue, Suite 2000, Seattle, WA 981104. Such payments shall be used for recovery of the state’s fees and costs in investigating this matter, monitoring compliance with this Assurance of Discontinuance, future enforcement of the Consumer Protection Act, or for any lawful purpose in the discharge of the state’s Attorney General’s duties at the sole discretion of the Attorney General.

27

I. To the extent not already provided elsewhere, Intuit shall, upon request by the Oversight Committee, provide all documentation and information necessary for the Oversight Committee to confirm compliance with the Assurance. To the extent not already provided elsewhere, Intuit shall ensure that all communications with the Fund Administrator regarding the administration of the Settlement Fund shall include at least one representative of the Oversight Committee.

J. The Attorneys General shall have no liability whatsoever to Intuit, the Fund Administrator, or any Covered Consumer in connection with the administration of the Settlement Fund or for any action by Intuit or the Claims Administrator with respect to the monies deposited.

K. The Attorney General of the State of New York shall satisfy the reporting obligations of the States under Section 6050X of the Internal Revenue Code of 1986, as amended, with respect to Intuit’s payments hereunder. Intuit is fully responsible for the payment of its taxes, including in the event any deductions for amounts paid under this settlement agreement are disallowed, as well as any fines or penalties imposed by the Internal Revenue Service with respect to such taxes.

VII. Assurance Acknowledgements

A. Intuit, within seven (7) days of the Effective Date, (1) must submit to the Oversight Committee an acknowledgment of receipt of this Assurance sworn under penalty of perjury; and (2) must identify to the Oversight Committee the primary physical, postal, and email address and telephone number, as designated points of contact, that the Oversight Committee may use to communicate with Intuit.

B. For five (5) years after the Effective Date, Intuit must deliver a copy of this Assurance to (1) all principals, officers, and directors; (2) all employees having managerial

28

responsibilities for Advertisements for any TurboTax Free Edition Product; the online search and search engine optimization strategies and practices for any TurboTax Free Edition Product and any TurboTax Paid Product; the representations made on the TurboTax Website regarding any TurboTax Free Edition Product; and customer service inquiries regarding any TurboTax Free Edition Product; and (3) any business entity resulting from any change in structure as set forth in the Section titled Compliance Reporting. Delivery must occur within seven (7) days of the Effective Date for current personnel. For all others, delivery must occur before they assume their responsibilities.

C. From each individual or entity to which Intuit delivered a copy of this Assurance, Intuit must obtain, within thirty (30) days, a signed and dated acknowledgment of receipt of this Assurance.

VIII. Compliance Reporting

A. One (1) year after the Effective Date, Intuit must submit to the Oversight Committee a compliance report, sworn under penalty of perjury, in which Intuit must identify all of Intuit’s tax preparation businesses by all of their names, telephone numbers, and physical, postal, email, and Internet addresses and describe in detail whether and how Intuit is in compliance with each Section of this Assurance.

B. For five (5) years after the Effective Date, Intuit must submit to the Oversight Committee a compliance notice, sworn under penalty of perjury, within fourteen (14) days of any change in the following: (a) any designated point of contact; or (b) the structure of Intuit that may affect compliance obligations arising under this Assurance, including: creation, merger, sale, or dissolution of the entity or any subsidiary, parent, or affiliate that engages in any acts or practices subject to this Assurance.

29

C. Intuit must submit to the Oversight Committee notice of the filing of any bankruptcy petition, insolvency proceeding, or similar proceeding by or against Intuit within fourteen (14) days of its filing.

D. Any submission to the Oversight Committee required by this Assurance to be sworn under penalty of perjury must be true and accurate, such as by concluding: “I declare under penalty of perjury under the laws of the United States of America that the foregoing is true and correct. Executed on: _____” and supplying the date, signatory’s full name, title (if applicable), and signature.

E. Unless otherwise directed by a representative of the Oversight Committee in writing, all submissions to the Oversight Committee pursuant to this Assurance must be made in accordance with the terms in Sections XII(L) and (M). All submissions shall have a subject line that must begin: Attorneys General v. Intuit Inc.

IX. Recordkeeping

Intuit must create certain records for ten (10) years after the Effective Date, and retain each such record for five (5) years. Specifically, Intuit must create and retain the following records:

A. Accounting records showing: (1) the revenues from all TurboTax Paid Products and any add-on products such as Audit Defense; and (2) the revenues from all TurboTax Paid Products and any add-on products such as Audit Defense that were received from consumers who began the process of preparing their returns in any TurboTax Free Edition Product;

B. Records of all consumer complaints and refund requests concerning the subject matter of this Assurance, whether received directly or indirectly, such as through a third party, and any response;

30

C. All records necessary to demonstrate full compliance with each provision of this Assurance, including all submissions to the Oversight Committee; and

D. To the fullest extent possible, a copy of each unique Advertisement or other marketing material relating to any TurboTax Free Edition Product.

X. Compliance Monitoring

A. For a period of five (5) years, and for the purpose of monitoring Intuit’s compliance with this Assurance: Within thirty (30) days of receipt of a written request from the Oversight Committee, Intuit must submit additional compliance reports or other requested information, which must be sworn under penalty of perjury.

B. Nothing in this Assurance limits any State’s lawful use of compulsory process, pursuant to applicable state law.

XI. Releases

A. By execution of this Assurance, and upon Intuit’s compliance with its terms including the payments required in Section VI, the States release and forever discharge Intuit and its past and present officers, directors, employees, agents, affiliates, parents, subsidiaries, operating companies, predecessors, assigns, and successors from all civil consumer-protection or unfair-trade-practices claims each Attorneys General is authorized by law to bring that arise from or relate to the findings contained herein.

B. Nothing contained in this Assurance shall be construed to limit the ability of any Attorney General to enforce the obligations that Intuit has under this Assurance. Further, nothing in this Assurance shall be construed to waive or limit any private rights of action.

C. Notwithstanding the releases in Subsection A of this Section, or any other term of this Assurance, the following claims are specifically reserved and not released by this Assurance: (1) claims based on violations of securities laws, including claims based on the offer, sale, or

31

purchase of securities; (2) claims of regulatory agencies having specific regulatory jurisdiction that are separate and independent from the regulatory enforcement of the Attorneys General; and (3) claims that arise from Intuit’s actions that take place after the Effective Date.

XII. General Provisions

A. The Parties understand and agree that the Attorneys General have defined jurisdiction under the laws, or assert jurisdiction under the common law, of their respective States for the enforcement of state Consumer Protection Acts.

B. The Parties understand and agree that this Assurance shall not be construed as an approval or sanction by the Attorneys General of Intuit’s business practices, nor shall Intuit represent that this Assurance constitutes an approval or sanction of its business practices. The Parties further understand and agree that any failure by the Attorneys General to take any action in response to information submitted pursuant to this Assurance shall not be construed as an approval or sanction of any representations, acts, or practices indicated by such information, nor shall it preclude action thereon at a later date.

C. Nothing in this Assurance shall be construed as relieving Intuit of the obligation to comply with all applicable state and federal laws, regulations, and rules, nor shall any of the provisions of this Assurance be deemed to be permission to engage in any acts or practices prohibited by such laws, regulations, and rules.

D. To the extent that there are any, Intuit agrees to pay all court costs associated with the filing (if legally required) of this Assurance by any State. No court costs, if any, shall be taxed against any State.

E. This Assurance may be executed by any number of counterparts and by different signatories on separate counterparts, each of which shall constitute an original counterpart thereof and all of which together shall constitute one and the same document. One or more

32

counterparts of this Assurance may be delivered by facsimile or electronic transmission with the intent that it or they shall constitute an original counterpart thereof.

F. This Assurance contains the complete agreement between the Parties. The Parties have made no promises, representations, or warranties other than what is contained in this Assurance. This Assurance supersedes any prior oral or written communications, discussions, or understandings.

G. For the purposes of construing the Assurance, this Assurance shall be deemed to have been drafted by all Parties.

H. This Assurance may not be amended except by an instrument in writing signed on behalf of all Parties to this Assurance.

I. This Assurance is entered into voluntarily and solely for the purpose of resolving the claims and causes of action against Intuit. Each Party and signatory to this Assurance represents that it freely and voluntarily enters into this Assurance without any degree of duress or compulsion.

J. Any failure by any Party to this Assurance to insist upon the strict performance by any other Party of any of the provisions of this Assurance shall not be deemed a waiver of any of the provisions of this Assurance, and such Party, notwithstanding such failure, shall have the right thereafter to insist upon the specific performance of any and all of the provisions of this Assurance.

K. If any clause, provision, or section of this Assurance shall, for any reason, be held illegal, invalid, or unenforceable, such illegality, invalidity, or unenforceability shall not affect any other clause, provision, or section of this Assurance, which shall be construed and enforced

33

as if such illegal, invalid, or unenforceable clause, section, or provision had not been contained herein.

L. Whenever Intuit shall provide notice to any Attorneys General under this Assurance, that requirement shall be satisfied by sending notice to the email and postal address for each respective Attorneys General identified in Appendix B in accordance with the following paragraph.

M. All notices or other documents to be provided under this Assurance shall be sent by U.S. mail, certified mail return receipt requested, or other nationally recognized courier service that provides for tracking services and identification of the person signing for the notice or document, and shall have been deemed to be sent upon mailing. Additionally, any notices or documents to be provided under this Assurance shall also be sent by electronic mail if an email address has been provided for notice. Any party may update its address by sending written notice to the other party.

N. If a court of competent jurisdiction determines that Intuit has breached this Assurance, Intuit shall pay to the Attorneys General the cost, if any, of obtaining such determination and of enforcing this Assurance, including without limitation legal fees, expenses, and court costs.

IN WITNESS WHEREOF, this Assurance is executed by the Parties hereto on the dates set forth below:

[Parties’ signature pages continued in the following pages]

34

For Intuit Inc.

By: /s/ Gregory N. Johnson

Date: April 28, 2022

Gregory N. Johnson

Executive Vice President and General Manager

Executive Vice President and General Manager

35

For New York State Attorney General Letitia James

LETITIA JAMES

Attorney General of the State of New York

28 Liberty Street

New York, NY 10005

By: /s/ Clark P. Russell

Date: May 4, 2022

Clark P. Russell

Deputy Bureau Chief

Deputy Bureau Chief

Bureau of Internet and Technology

By: /s/ Joseph P. Mueller

Date: May 4, 2022

Joseph P. Mueller

Assistant Attorney General

Bureau of Consumer Frauds and Protection

36

Appendix A – “Free, Free, Free” Advertisements5

•“Big Kick”

o The “Big Kick” advertisement depicts a high school football placekicker and his supportive father. In the moments before an important kick, the son flashes back to a memory from his youth of his father encouraging him; returning to the present, the son converts the field goal attempt while his father looks on. However, instead of featuring conventional dialogue, the characters in “Big Kick” repeat only the word “free” throughout the ad.

•“Credits”

o In the “Credits” advertisement, a John McClane-type action hero utters a wisecrack (here, the word “free” several times) as he drops a lighter onto a streak of gasoline, which triggers the explosion of a batter white van. As flames explode into the air, the action hero strides towards the camera in slow motion, prompting

5 This Appendix addresses all versions of the listed advertisements, i.e., 15-second, 30-second, and 60-second versions of the advertisements, to the extent they exist.

A-1

the credits to roll on screen, with every actor and role consisting of one or more uses of the word “free.”

•“Crossword”

o In “Crossword,” a white-haired couple completes a crossword puzzle in which every clue and every answer is one or more uses of the word “free.”

A-2

•“Game Show”

o The “Game Show” advertisement depicts a 70s-era game show in which a woman must guess what activity or concept her male partner is miming. Every one of the woman’s answers is correct and consists of one or more uses of the word “free.”

•“Lawyer”

o In “Lawyer,” an attorney delivers an impassioned closing argument to the jury as dramatic music swells, with every word of the attorney’s argument being “free.”

A-3

After he finishes, a member of the jury leads a standing ovation, as various jurors repeat the word “free” several times.

•“Spelling Bee”

o The “Spelling Bee” advertisement shows a middle school-aged boy correctly spelling the word “free” in a spelling bee. Aside from the boy’s spelling out the letters “F-R-E-E,” every line dialogue spoken by the boy and by the judge of the spelling bee consists entirely of the word “free.”

A-4

•“Echo”

o In “Echo,” a hiker shouts “free” from the top of a mountain, with the word “free” reverberating back to her as a result.

A-5

•“Auctioneer”

o In “Auctioneer,” a fleet-tongued auctioneer rattles off prices and bids to a collection of ranchers and cowboys. Instead of conventional dialogue, the auctioneer repeatedly utters the word “free.”

A-6

•“Dance Workout”

o The “Dance Workout” advertisement depicts an instructor leading an enthusiastic dance workout class. Instead of conventional words of encouragement and instruction, the instructor repeats the word “free.”

A-7

Appendix B – State Notices

| Alaska |

1031 West 4th, Ave., Suite 200

Anchorage, AK 99501

consumerprotection@alsaka.gov

|

||||

| Alabama |

501 Washington Avenue

Montgomery, AL 36130

Olivia.Martin@AlabamaAG.gov

|

||||

| Arkansas |

323 Center Street, Suite 200

Little Rock, AR 72201

|

||||

| Arizona |

Alyse Meislik

Consumer Protection & Advocacy Section

2005 N. Central Ave.

Phoenix, AZ 85004

Alyse.Meislik@azag.gov

consumer@azag.gov

|

||||

| California |

300 South Spring Street, Suite 1702

Los Angeles, CA 90013

bernard.eskandari@doj.ca.gov

|

||||

| Colorado |

1300 Broadway

Denver, CO 80203

abigail.hinchcliff@coag.gov

|

||||

| Connecticut |

Brendan T. Flynn, AAG

Office of the Connecticut Attorney General

165 Capital Ave.

Hartford, CT 06106

Brendan.Flynn@ct.gov

|

||||

| District of Columbia |

Office of Consumer Protection

Public Advocacy Division

ATTN: Tim Shirey, Investigator

D.C. Office of the Attorney General

400 6th Street NW

Washington D.C. 20001

Timothy.Shirey@dc.gov

|

||||

| Delaware |

820 N. French St., 5th Floor

Wilmington, DE 19801

katherine.devanney@delaware.gov

|

||||

| Florida |

Edward Moffitt

Chief Investigator, MSPB & Cyber Fraud Bureau

Office of the Florida Attorney General

135 West Central Boulevard, Suite 670

Orlando, FL 32801

Edward.Moffitt@myfloridalegal.com

|

||||

A-8

| Georgia |

2 Martin Luther King, Jr. Drive, Suite 356E

Atlanta, GA 30334

dzisook@law.ga.gov

|

||||

| Hawaii |

235 S. Beretania Street #801

Honolulu, Hawaii 96813

ltong@dcca.hawaii.gov

rtolenti@dcca.hawaii.gov

|

||||

| Illinois |

100 W. Randolph St., 12th Fl.

Chicago, IL 60601

Daniel.edelstein@ilag.gov

|

||||

| Iowa |

William Pearson

Iowa Department of Justice

1305 E. Walnut, 2nd Floor

Des Moines, IA 50319

William.pearson@ag.Iowa.gov

|

||||

| Idaho |

P.O. Box 83720

Boise, ID 83720-0010

stephanie.guyon@ag.idaho.gov

|

||||

| Indiana |

302 W. Washington St.

IGCS, 5th Floor

Indianapolis, IN 46204

Michelle.Alyea@atg.in.gov

|

||||

| Kansas |

120 SW 10th Avenue, 2nd floor

Topeka, KS 66612

sarah.dietz@ag.ks.gov

|

||||

| Kentucky |

1024 Capital Center Drive, Suite 200

Frankfort, KY 40601

Christian.Lewis@ky.gov

|

||||

| Louisiana |

1885 N 3rd Street

Baton Rouge, LA 70802

MughalA@ag.louisiana.gov

|

||||

| Massachusetts |

One Ashburton Place, 18th Floor

Boston, MA 02108

Glenn.kaplan@mass.gov

|

||||

A-9

| Maryland |

Consumer Protection Division of the Office of the Attorney General of Maryland

Elizabeth Stern

Assistant Attorney General

200 Saint Paul Place

Baltimore, MD 21202

estern@oag.state.md.us

With a copy to:

Chief, Consumer Protection Division

200 Saint Paul Place

Baltimore, MD 21202

consumer@oag.state.md.us

|

||||

| Maine |

6 State House Station

Augusta, Maine 04333-0006

christina.moylan@maine.gov

|

||||

| Michigan |

525 W. Ottawa St.

PO Box 30736

Lansing, MI 48909

Levina@michigan.gov

|

||||

| Minnesota |

445 Minnesota Street, Suite 1200

Saint Paul, MN 55101

alex.baldwin@ag.state.mn.us

|

||||

| Missouri |

815 Olive Street, Suite 200

St. Louis, MO 63101

Michael.Schwalbert@ago.mo.gov

with an additional hard copy to: 207 W. High St.

P.O. Box 899

Jefferson City, MO 65102

|

||||

| Mississippi |

Post Office Box 220

Jackson, MS 39205

caleb.pracht@ago.ms.gov

consumer@ago.ms.gov

|

||||

| Montana |

215 N Sanders Street

Helena, MT 59601

ocpinvestigations@mt.gov

|

||||

| North Carolina |

PO Box 629

Raleigh, NC 27602

|

||||

A-10

| North Dakota |

1720 Burlington Drive, Suite C

Bismarck, ND 58504-7736

pgrossman@nd.gov

|

||||

| Nebraska |

2115 State Capitol Building

Lincoln, NE 68509

michaela.hohwieler@nebraska.gov

|

||||

| New Hampshire |

33 Capitol St.

Concord, NH 03301

|

||||

| New Jersey |

124 Halsey St. - 5th Floor

P.O. Box 45029

Newark, NJ 07102

monica.finke@law.njoag.gov

zeyad.assaf@law.njoag.gov

|

||||

| New Mexico |

Lawrence Otero

Brian McMath

Assistant Attorneys General

Consumer & Environmental Protection Division

New Mexico Office of the Attorney General

P.O. Box 1508

Santa Fe, New Mexico 87504

lotero@nmag.gov

bmcmath@nmag.gov

|

||||

| Nevada |

100 North Carson Street

Carson City, NV 89701

MNewman@ag.nv.gov

and

8945 W. Russell Road, Suite 204

Las Vegas NV 89148

Sforbes@ag.nv.gov

|

||||

| New York |

28 Liberty St.

New York, NY 10005

joseph.mueller@ag.ny.gov

clark.russell@ag.ny.gov

|

||||

| Ohio |

1 Government Center

640 Jackson St., Suite 1340

Toledo, Ohio 43604

Timothy.Effler@OhioAGO.gov

|

||||

| Oklahoma |

313 NE 21st St.

Oklahoma City, OK 73105

Malisa.McPherson@oag.ok.gov

|

||||

A-11

| Oregon |

Oregon Department of Justice

Attn: Althea Cullen, AAG

100 SE Market Street

Portland, OR 97201

Althea.d.cullen@doj.state.or.us

|

||||

| Pennsylvania |

John Abel

Assistant Director for Multistate and Special Litigation

Pennsylvania Office of Attorney General

15th Floor, Strawberry Square

Harrisburg, PA 17120

jabel@attorneygeneral.gov

|

||||

| Rhode Island |

150 South Main St.

Providence RI 02903

sprovazza@riag.ri.gov

|

||||

| South Carolina |

P.O. Box 11549

Columbia, SC 29211

rhartner@scag.gov

|

||||

| South Dakota |

1302 E. Hwy 14, Suite 1

Pierre, SD 57501

Consumerhelp@state.sd.us

|

||||

| Tennessee |

PO Box 20207

Nashville, TN 37202-0207

Kelley.groover@ag.tn.gov

|

||||

| Texas |

PO Box 12548 (MC-010)

Austin, Texas 78711

patrick.abernethy@oag.texas.gov